Housing market: build back better for the long-term

We are likely to face another decade of quantitative easing and ultra-low interest rates. In our view, this is creating housing market bubbles, especially in the core of the Eurozone, like in Germany for example.

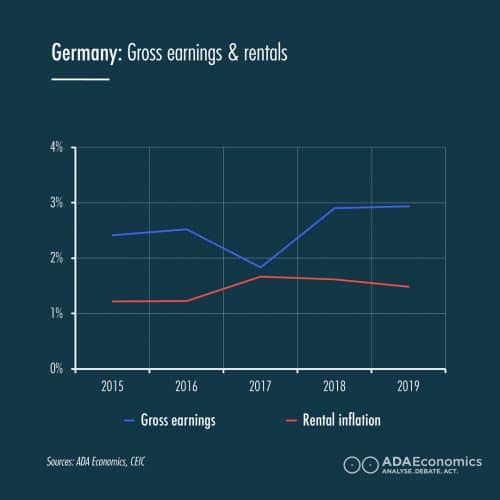

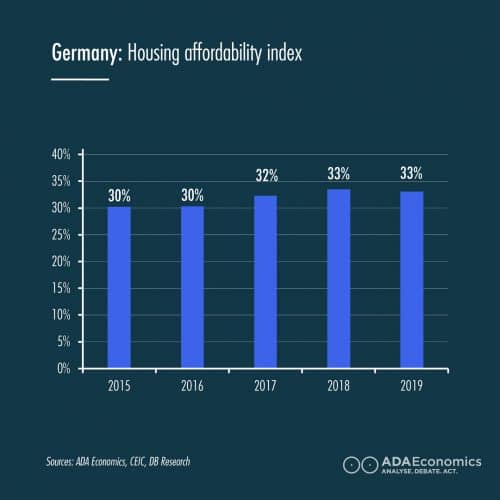

In the last 5 years, German nominal wages growth has exceeded rents inflation. However, our housing affordability index shows that affordability of housing worsened because more a rising share of earnings was needed to repay the mortgage. We created simple calculations to measure the affordability of the housing market (on average) taking into consideration the fluctuation in average square meter residential housing, the (dropping) retail mortgage rates and wage growth (again measured by the national average index).

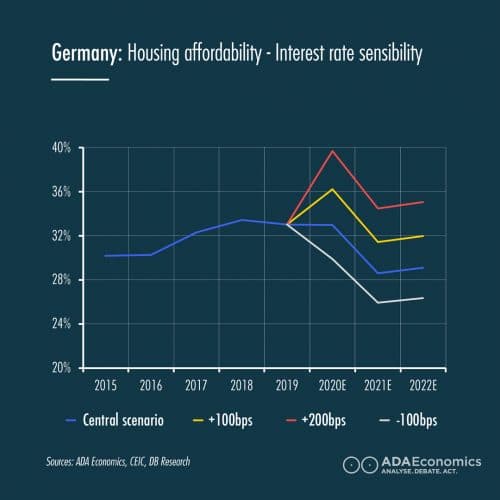

Going forward, affordability should have improved if house prices (and rents) were to drop in line with the expected contraction in GDP.

Data and methodology: Annual average inflation rate for actual rental for housing (2015-2019); and annual average gross earnings (2015-2019)

Data and methodology: Affordability index is estimated using average wages, house purchase prices and long-term lending rates for house purchase

However, there is growing risk that Central Bank’s desperate desire to push for a rapid recovery will limit the drop in house prices and thus affordability may not improve by much, especially since the labour market is going to weaken everywhere, even in Germany.

There is also another problem in the background: the more we stimulate the recovery via debt, the more it will become evident that monetary policy does not face constrains on the way DOWN (that is limits to its ability to stimulate the recovery when interest rates are near zero) but rather on the way UP (that is their inability of keeping an economic recovery on track through an even minor interest rate tightening cycle). Look at the huge jump in the mortgage burden if mortgage rates were to rise 200bps next year (which would mean a mortgage goes from an interest rate of around 1.1% to 3.1% p.a.)

Build back better – should imply policies designed to build economic models that can withstand decades, not just a few years.