The wage convergence process within the European Union is ongoing and has accelerated partly because of the different depths of the recession within the EU. This process sees a structural increase favouring incomes in those countries that are “poorer than the EU average” – meaning their average income is below the EU average – that is many of the new Euro member states. At the same time, convergence implies that the countries with average income above the mean face strong headwinds to compress incomes, on average, and particularly in certain segments of society. The most vulnerable country at the moment on the way down is Italy, and it is also the country where the downward force was probably accentuated by COVID-19, as it has a high number of self-employed people and this part of the labour force was hit heavily by the shutdowns.

The convergence process in Europe reflects the strength of the single market framework, the impact of the EU cohesion funds strategy and the evolution of policy making in the EU. These three factors have resulted in the continuing relocation of manufacturing production eastwards, which is likely to continue, even once average incomes in Italy move evidently below the central and eastern European countries, if the current policy strategies in each member state remain intact.

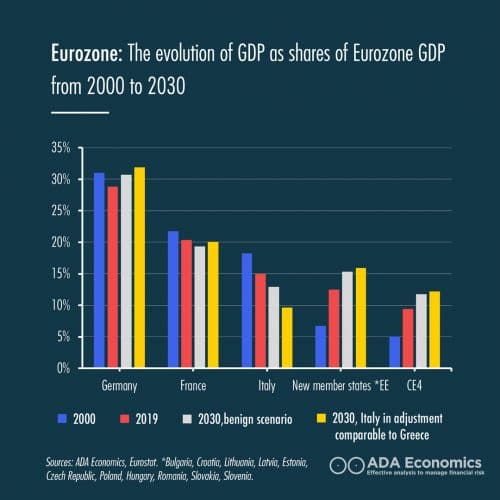

To give you a sense of how powerful this process is for the internal politics of the EU, we have charted, below, the weight of the GDP of various member states relative to Eurozone GDP: of Germany, France, Italy and the combination of the CE4, as well as all the member states that have joined since 2004 (bar Malta and Cyprus, as they have different business models). We project the GDP until 2030 by simply keeping the average growth of the past decade unchanged – which appears to be a fairly unbiased assumption – and including Bulgaria and Croatia in the eurozone GDP projection given their recent entry in the ERM2 system and the high odds they will fulfil the requirements for full euro adoption in 2023. In the benign scenario, Italy manages to grow the economy in nominal terms by 1.3% on average, the same as the past decade; while, in a less favourable scenario, the average GDP is negative as we believe that, at some point, the economy will go through an adjustment phase similar to what has been experienced by Greece (regardless of whether this is associated with a Troika programme or not). We suspect that the less benign scenario is the more realistic one. That said, even in a better scenario, the share of Italian GDP in the EU drops materially and will most certainly be lower than the CE4 combined, and meaningfully lower than the aggregate GDP of the newer member states. This necessarily implies a profound change in income prospects and the further erosion of political influence by Italy.

We put forward some ideas to support the recovery of Italy – check them out and share your opinion with us!