We see the dispute between Europe, the US and Russia as a long-lasting one, which is likely to continue to deliver small but incremental sanctions on Russia for many more years. The announcement on 18 February by Federica Mogherini, the High Representative of the European Union for Foreign Affairs and Security Policy, fits this picture. The EU member states have reached a political consensus for the new sanctions against Russia, following the Kerch Strait incident with Ukraine. This new batch of sanctions is likely to be targeted at individuals believed to be connected with the incident, and not companies or sectors of the Russian economy.

The Kerch Strait divides the Black Sea from the Sea of Azov, shared by Russia and Ukraine. In 2018, Russia completed a bridge to connect Ukraine with the Russian mainland, which deteriorated the feeble balance of the area. From the Russian federation’s perspective, on 26 November, Ukrainian military ships crossed Russian territorial waters illegally; while, according to the Ukrainian side, the vessels had requested the permits, but did not receive answers from the Russian administration. As a result, the three Ukrainian military ships ready to enter the Sea of Azov were seized by the Russian Navy, with the 24 sailors on the ships awaiting trial in Moscow currently.

As the US and Europe introduce more sanctions, Russia retaliates implicitly. Last year, President Vladimir Putin unveiled several new types of state-of-the-art weapons, and their existence and intent was clearly included in his recent annual State of the Nation address. The arrest of American private equity investor Michael Calvey may also be part of the implicit retaliation.

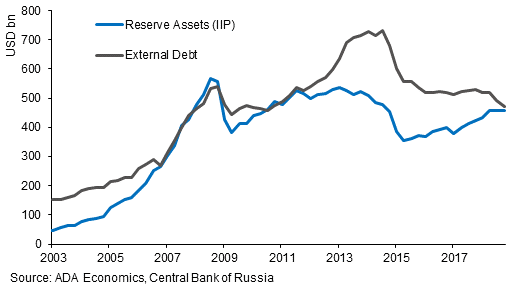

Additional sanctions are also due from the US Congress this year. In our view, a total ban on US ownership of Russian local debt appears unlikely to us, given the increasingly bolder responses from Russia. Currently, foreign ownership of Russian local debt is worth USD 27bn – total liquidation would not be a major problem for the economy as a whole (the current account surplus reached 7% of GDP in 4Q18), but it would weigh on the currency perhaps as much as a further 15% depreciation, which would prove short-lived this time, in our view, as too much currency weakness does not appear desirable for internal stability. In his State of the Nation address, President Putin signalled that fiscal support for families and the poorest will increase, and promised lower borrowing costs and tax breaks for construction. This is consistent with our view that Russia is transiting towards a low inflation, low interest rates economy, and the CBR is likely to resume its monetary easing by the year-end.